Buy Now Pay Later (BNPL) services have changed how people shop, making online purchases feel less risky and, perhaps, more manageable.

These payment platforms — Klarna, Afterpay, Affirm, and Clearpay — let buyers split up costs over time, often with no interest. For many, this flexibility is appealing.

But it’s worth diving into what sets each apart, as the best BNPL solution depends on someone’s shopping habits, locations, and, perhaps, their comfort level with deferred payments.

This article explores the core similarities and subtle differences among Klarna, Afterpay, Affirm, and Clearpay.

If you’ve ever hesitated at a checkout page, unsure of which option to choose, or wondered how splitting payments might affect your budget or credit, the following insights can help clarify your decision.

The goal? To help everyday shoppers — whether students, parents, or professionals — make responsible, informed choices while enjoying a bit more financial breathing room.

What Is Buy Now Pay Later and How Does It Work?

BNPL services allow customers to purchase goods and spread the cost into regular payments. Most often, there are no added fees or interest, provided payments are on time.

Instead of using a credit card, a shopper can simply select BNPL at checkout. It sounds straightforward, but different companies structure these offers in unique ways, and even the same provider can vary its approach by region or retailer partnerships.

These platforms have become especially popular with online clothing and tech purchases — not surprising, since large upfront costs can make customers hesitate.

The majority of BNPL services run light credit checks or none at all for smaller purchases, so they’re accessible even to those without traditional credit cards.

Still, late payments can result in penalties, and users worried about debt should review terms closely.

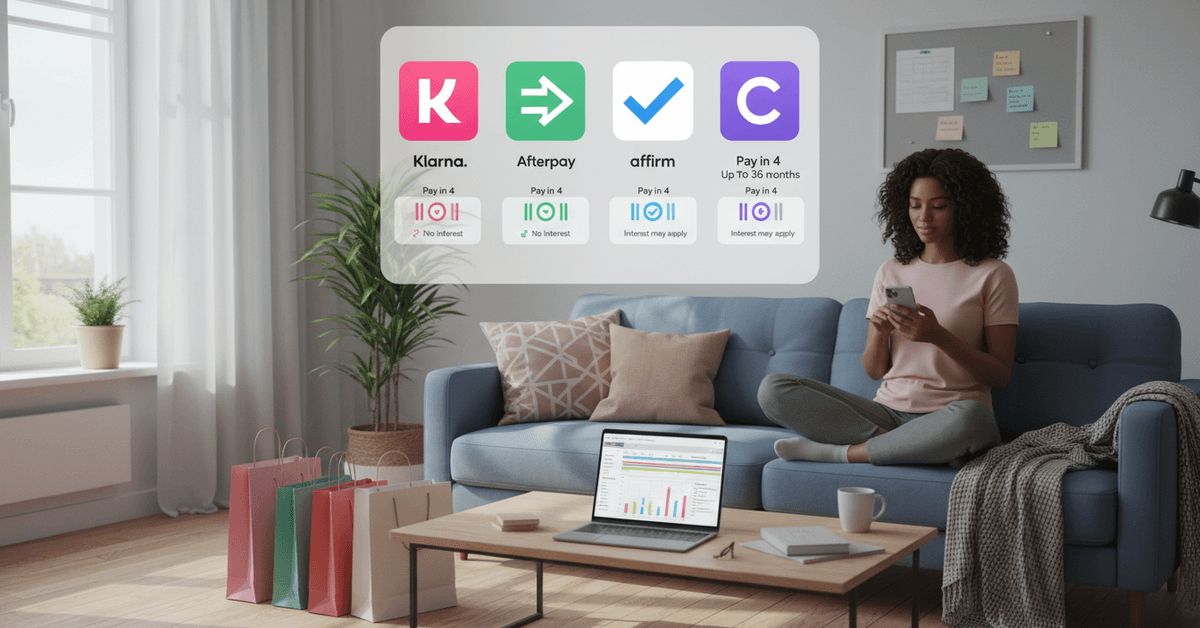

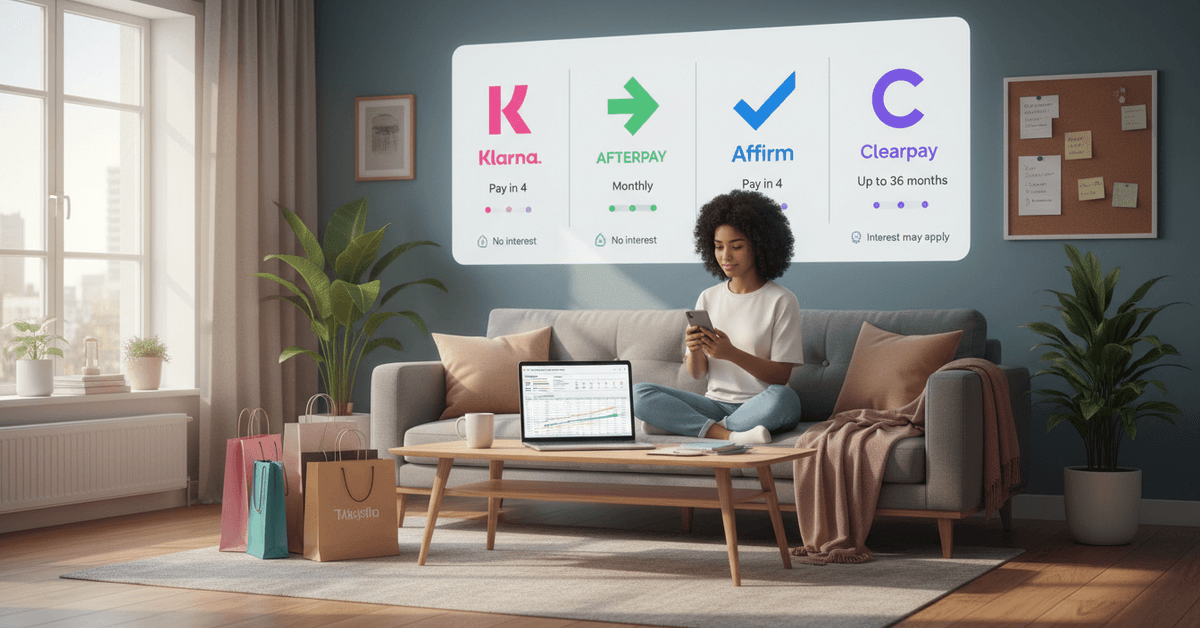

Klarna vs Afterpay vs Affirm vs Clearpay: Overview Table

Each platform has standout features, but for quick comparison, see the table below.

Platform Overviews: Key Features at a Glance

Klarna

Klarna started in Sweden and is now a global name in BNPL. It offers a variety of payment plans, including interest-free pay-in-4, longer-term financing, and even direct payments.

Some customers enjoy Klarna's app, which brings spending tracking and even some exclusive discounts. One small thing: Klarna runs a soft credit check for certain longer plans, so not all purchases are instantly approved.

It’s easy to lose track of payments, especially when using multiple merchants — something to watch out for.

Afterpay

Afterpay, which began in Australia, has built its name on simplicity. Shoppers usually split payments into four fortnightly installments, with no interest applied if paid on time. Late fees are capped and transparent.

Afterpay partners with fashion and lifestyle brands, making it a favorite for people who shop regularly in those areas. The service doesn’t generally perform hard credit checks, making it accessible to younger buyers.

Some users may, perhaps, feel too tempted to overspend, given how effortless installment approval can seem.

Affirm

Affirm is based in the US and takes a slightly different approach. It provides short-term, interest-free options on smaller purchases, and longer-term plans (sometimes up to 36 months) with interest displayed up front.

Affirm’s model is transparent — users always see the total interest before accepting. Sometimes, this service reports payments to credit bureaus, which means responsible use might help build a credit profile.

However, the possibility of paying interest should probably push users to compare total costs before clicking 'accept.'

Clearpay

Clearpay is the UK version of Afterpay (owned by the same company), so its core service is nearly identical: pay-in-4 installments, interest-free as long as payment deadlines are met.

It's particularly popular with millennial and Gen Z shoppers in the UK and Europe. Like Afterpay, Clearpay won’t typically do a hard credit check and instead limits spending based on ongoing repayment habits.

While many find Clearpay simple to use, refunds and dispute resolutions can sometimes feel slower, depending on merchant policies.

Eligibility: Who Can Use BNPL Services?

Most BNPL platforms require shoppers to be over 18, have a valid bank card, and live in a supported country.

Klarna and Affirm offer broader international availability, while Afterpay and Clearpay focus more on Oceania, North America, and the UK, respectively. Specific eligibility rules — like requiring a residential address or placing caps on first-time users — can differ slightly.

Perhaps unsurprisingly, companies routinely update policies to align with local regulations, so checking current requirements is wise.

Credit Checks and Approval Process

Klarna and Affirm sometimes conduct soft or hard credit checks for larger amounts or extended payment terms. Afterpay and Clearpay almost never do.

This makes the latter two appealing to those with thin credit histories or who want to avoid inquiries. However, the flip side is that spending limits can be stricter until a good repayment track record is built.

Main Features Compared: Payment Plans, Interest, and Fees

It’s easy to focus only on the payment schedule, but hidden fees and interest can occasionally catch buyers by surprise.

Here’s how each company handles these aspects.

Payment Schedules

- Klarna : Offers pay-in-4, monthly financing, or pay-in-30-days options.

- Afterpay : Standard pay-in-4 installments over six weeks.

- Affirm : Pay-in-4 for short terms; longer options (3-36 months) for bigger purchases.

- Clearpay : Pay-in-4 over six weeks, similar to Afterpay.

Interest Rates

- Klarna : Interest-free on pay-in-4 and pay-in-30, but financing plans may charge interest (APR varies).

- Afterpay : No interest. Instead, late fees apply if payments are missed.

- Affirm : Some plans are interest-free, others display fixed APRs (up to 36%).

- Clearpay : No interest on pay-in-4. Late fees apply, but are limited.

Late Fees and Penalties

- Klarna : Late fees vary by country but are generally capped.

- Afterpay : Capped late fees, usually up to 25% of purchase value.

- Affirm : Rarely charges late fees; instead, may freeze account or reduce spending limits.

- Clearpay : Late fees, clearly stated at checkout, with a maximum limit.

User Experience: App Design, Support, and Flexibility

Mobile Apps and Tracking

All four offer highly rated mobile apps. Klarna’s app tends to lead in extra features, like curated deals or in-app browsing.

Afterpay and Clearpay focus on simplicity, and Affirm’s interface is praised for its upfront loan terms and timeline displays. Not everyone wants too many bells and whistles — some users say the flood of reminders can be overwhelming.

Customer Support

Most platforms offer email and chat support, but not all provide phone numbers. Klarna and Affirm update FAQs and resource articles frequently; Afterpay and Clearpay can sometimes feel less responsive at peak times, based on some anecdotal reviews.

Still, most problems — like payment rescheduling or refund requests — are handled easily through each app or website.

Returns and Refunds

In theory, returning an item and reversing a BNPL payment should be easy. In practice, refunds often hinge on the merchant’s speed. Affirm and Klarna tend to process refunds once the merchant approves.

Afterpay and Clearpay might keep an installment due until the refund clears, which may inconvenience shoppers occasionally. If managing cash flow is a top concern, it’s worth noting that delays can happen.

Availability: Where Are Klarna, Afterpay, Affirm, and Clearpay Used?

Klarna and Affirm feature broad merchant networks in North America and Europe, though Klarna reaches more European brands and Affirm more US ones.

Afterpay and Clearpay anchor their presence in Australia, New Zealand, the UK, and, for Afterpay, the US and Canada. For shoppers who travel or buy from retailers abroad, selecting a service with wider retailer coverage could be more beneficial.

Shoppers’ Concerns: Credit Impact and Budgeting

Credit Score Effect

Most BNPL providers do not report everyday pay-in-4 activity to major credit bureaus. Affirm sometimes reports longer-term loans, and Klarna recently began reporting certain activities in select regions (like the UK).

For shoppers aiming to boost credit, only some BNPL plans will make a difference. Overdue payments, however, can eventually reach collections and harm scores, though policies change and may vary per country.

Budgeting Risks

Splitting large purchases across multiple platforms can quietly become overwhelming. The ease of approval sometimes encourages people to take on more than they realize — especially when payments are staggered.

For those uncertain about their own discipline, sticking to one platform and tracking upcoming dues is a safer course. Some friends have told stories of missing payments simply because one too many reminders blurred together.

It happens. Using available in-app budgeting tools, calendar links, or simple reminders can help.

BNPL Pros and Cons: At a Glance

- Advantages: Flexible payment schedules. No interest (for most pay-in-4 plans). Easy approval. Popular at many major retailers. User-friendly apps.

- Drawbacks: Late payment fees. Can encourage overspending. Credit score impact (rare, but possible). Refund delays with some retailers.

Which BNPL Platform Might Suit Your Needs?

Choosing among Klarna , Afterpay , Affirm , and Clearpay sometimes comes down to where you shop, your location, and how disciplined you are with payments.

People who value extras might appreciate Klarna’s app; those who want simple, tuition-style payment plans, Afterpay or Clearpay may appeal.

Affirm could be better for shoppers who might want the option of longer payment terms, or who care about up-front disclosure of any interest costs.

No platform is perfect. Yet, each offers a valuable way to spread costs and maybe—at times—enjoy a little less stress at checkout.