Searching for a credit card for bad credit can feel confusing, especially with new options emerging each year. By 2026, the landscape has shifted, offering fresh solutions for those seeking easy approval, even without a credit history.

If you’re dealing with bad credit or just starting out financially, finding a credit card without a credit check could offer a second chance—or perhaps, a first one.

This guide can serve readers who have struggled with past financial mistakes or those new to credit altogether. It explores the most accessible credit cards for all credit backgrounds, focusing on choices that avoid hard credit pulls.

There’s no judgment here—just facts, tips, and current information. Readers may find more options than expected, opening up flexible routes for building or repairing credit in 2026, while also handling payments safely.

Understanding Bad Credit and No Credit Check Cards

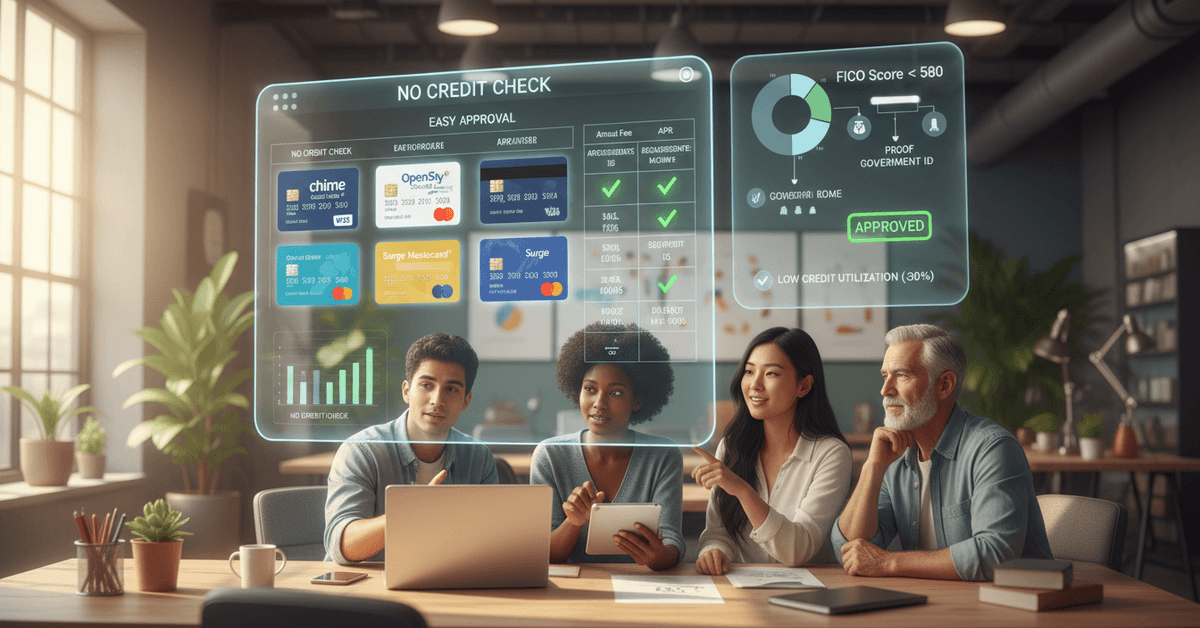

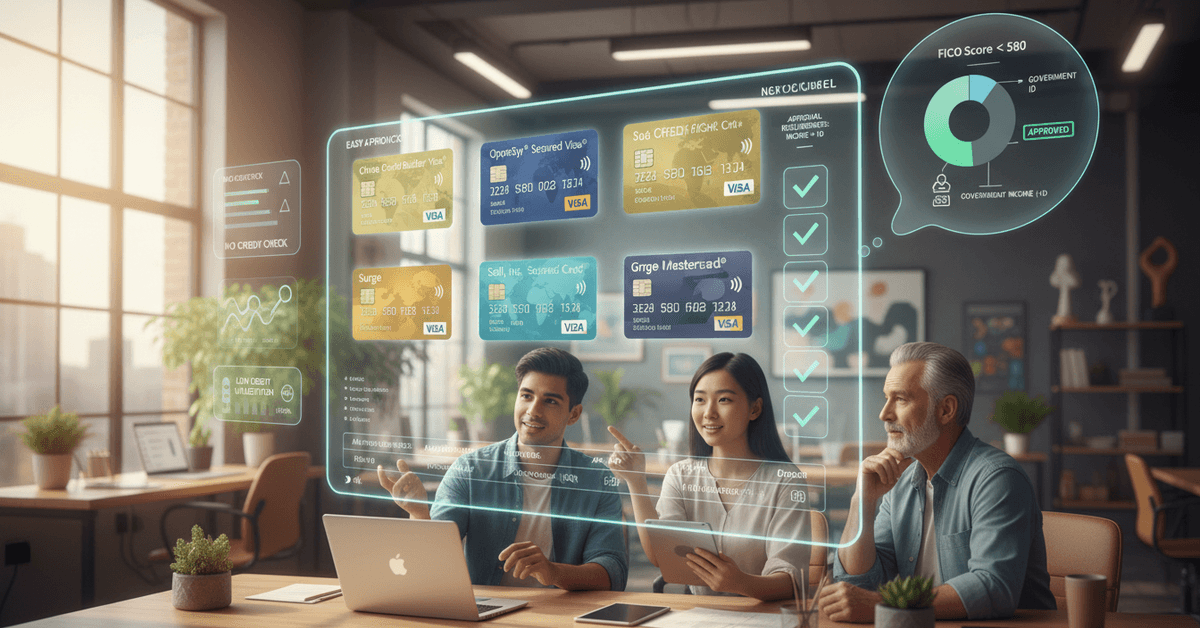

Before diving into the cards themselves, it may help to understand what ‘bad credit’ actually means. Generally, a credit score under 580 (FICO scale) is considered poor.

That said, sometimes people with no score at all face similar hurdles. Certain credit cards are marketed directly for those with bad credit, while others are designed for applicants with limited or no history.

No credit check or "soft pull" card options may appeal to anyone worried about rejection from traditional credit applications.

These cards avoid a hard inquiry, so an application won't lower your score or affect your history. However, the features and benefits tend to be different compared to mainstream credit products.

Balances, limits, and fees vary. It's good to weigh the pros and cons before jumping in—though some people find them their only realistic choice.

Why Consider a Credit Card with No Credit Check?

There are several reasons someone might prefer a no credit check credit card. For many, it could be about avoiding the embarrassment or frustration of repeated rejections. For others, it’s the anxiety about another dip in their already low score.

With these specialized cards, you might find that approval is based more on income or identification rather than credit history.

They may suit people recovering from bankruptcy, students without credit, or workers new to the country. Certain cards are even designed to help immigrants or people rebuilding after financial hardship.

Typical Features of No Credit Check Cards

- No hard pull on your credit report

- Quick and mostly automated approval decisions

- Lower credit limits at first, sometimes with the promise of increases after good behavior

- Annual fees—these may be higher than average, but some cards keep it reasonable

- Basic account features: online management, fraud protection, and sometimes rewards

Best Credit Cards for Bad Credit in 2026

The 2026 card landscape includes both new entrants and updated classics. Below are some notable options, each offering their own approach for people with bad credit or no history. It’s important to read the latest terms, since these can change.

1. Chime Credit Builder Visa® Card

Chime has gained traction for its promise of ‘no credit check’ and painless approval. The secured Chime Credit Builder card links to your Chime bank account.

There’s no annual fee, no interest, and any balance must be paid off monthly. For users with bad credit or none at all, this approach removes many common pitfalls.

2. OpenSky® Secured Visa® Credit Card

OpenSky remains a popular secured choice for 2026. The card skips the credit check entirely. Approval is income-based, with an initial deposit that becomes your credit line.

Responsible use is reported to major credit bureaus, supporting credit building efforts. The annual fee is present, but it’s often considered reasonable given the accessibility.

3. Self, Inc. Secured Credit Card

Self links its secured card to a credit-building loan. Applicants begin by opening a small “credit builder account.” No hard credit pull is required.

Once monthly payments accrue, a Self Visa® card becomes available as an optional add-on. It’s a gradual, structured approach that suits methodical users.

4. Surge Mastercard®

This card targets applicants with bad credit, promising a prequalification process that uses only a soft inquiry.

While not entirely free of fees or interest, the Surge Mastercard is designed to provide a quick answer and a path toward higher limits after several timely payments. Customers may want to watch fee structures closely.

5. Grow Credit Mastercard®

Grow Credit's model takes a creative approach. Instead of a security deposit or cash collateral, the Grow card is issued based on streaming and other subscription payments.

Approval hinges on current subscriptions rather than a credit check or traditional banking relationship. For some, this opens up a unique way to build credit incrementally.

Other Notable Options in 2026

- Secured Discover it®: Offers cash back, but the deposit is required and there’s usually a credit check. However, new 2026 pilots let some applicants apply with just a soft pull.

- Capital One Platinum Secured: Known for its tiered deposit system, a portion of users now qualify without a hard pull in 2026. Keep an eye out for these changes in eligibility.

How Approval Works: What to Expect in 2026

Even in 2026, the process of getting approved for a credit card with bad credit involves a few predictable steps.

Application times and experiences may vary, but with no credit check cards, the main focus shifts to things like steady income, US residency, and proper identification.

Some card issuers use proprietary algorithms to double-check risk factors, sometimes leading to quirky or unpredictable results. It isn’t always a science.

Traditional secured cards will request a deposit, typically ranging from $49 to $500. These deposits are nearly always refundable.

In contrast, fintech offerings like Chime or Grow might offer credit without a cash deposit, relying instead on a linked account or regular payment activity.

What to Watch For With Easy Approval Cards

- Annual and monthly fees: Can add up quickly without noticing.

- Interest rates: Even ‘starter’ cards can come with high APRs.

- Upgrade potential: Some cards will consider a limit increase or even switch to unsecured after a track record.

- Reporting: Not all cards report to all three bureaus. That affects your ability to build credit broadly.

Strategies for Building Credit Effectively

Simply getting a credit card for bad credit is only the first step. The real improvement comes with using that card thoughtfully. These habits can help:

- Always pay on time, even if you only use the card for small or recurring purchases.

- Keep balances low—ideally below 30% of your total limit.

- Avoid applying for too many cards at once, as multiple inquiries (even soft checks) may seem risky to some issuers.

- Monitor your statements and report errors immediately.

- Take advantage of autopay or alerts if you tend to forget payment dates.

Secured Vs. Unsecured: Which Is Right For You?

Secured cards require a deposit; unsecured do not. Many people start with secured cards when their credit is damaged. Unsecured cards without a credit check exist, but they’re rarer and often carry higher fees.

Over time, responsible use may open up more choices, including a switch to unsecured with the same provider. It’s a bit of a patience game, and opinions on which route is best may differ based on personal tolerance for fees and risk.

Comparing Top Credit Cards for Bad Credit 2026

Given the array of options, visual comparisons can be useful. A summary table—showing annual fees, deposit requirements, reporting habits, and unique features—usually makes differences quite clear.

Some readers might notice that, beyond headline features, the total cost of ownership is the key variable.

Common Fees and APRs

- Annual fees: Range from $0 to over $100 depending on card structuring.

- APR ranges: Typically higher, often 18%–29% for unsecured cards. Secured cards are sometimes more forgiving.

- Late payment fees: Can damage credit further and are best avoided through autopay or reminders.

Tips to Avoid Pitfalls with Bad Credit Credit Cards

Experience suggests that new cardholders with bad credit should be extra careful with spending, fees, and recurring payments.

Setting up a calendar alert for payments may seem unnecessary, but it’s easy to forget in daily life. It could be worth checking card statements each month for unexpected charges or errors.

- Limit your total number of cards

- Watch for hidden fees in the fine print, like processing or inactivity charges

- Use your card, but not excessively—a small recurring bill works well for this

- Review credit reports at least annually for signs of progress, or lingering negative marks

Legal and Regulatory Considerations for 2026

Credit card laws continue to evolve. By 2026, updated regulations support greater disclosure of rates and fees to users.

The Credit CARD Act reforms remain relevant, and newcomers like the Consumer Financial Protection Bureau provide up-to-date resources on fair lending and dispute resolution.

The use of AI and alternative data for credit decisions is growing. While this may unlock new products for some, others might worry about data privacy or new types of biases. Reviewing issuer privacy policies and considering which data is shared is never a bad idea.

Common Documentation and Compliance Steps

- Proof of income or employment: Often a requirement, especially for no credit check cards.

- Valid government ID: Required to confirm identity, especially when applying online.

- Social Security Number: Still required by most mainstream U.S. providers, even with no credit pull.

Final Thoughts on Credit Cards

Credit cards for bad credit or no credit check can offer a practical way to rebuild financial confidence in 2026. The best options usually focus on transparent fees, credit bureau reporting, and manageable limits.

Applicants should avoid high-cost cards, pay on time, and use credit only for small planned purchases. With consistent responsible use, these cards can become a helpful step toward stronger credit access.