Shoppers in 2026 might notice how store credit cards with 0% interest offers are everywhere. And honestly, who hasn’t been curious about saving money this way—even if just for a big holiday purchase?

This article digs into the details of retail financing, especially for those looking to stretch budgets or build credit. It’s especially useful for regular shoppers, deal hunters, or anyone seeking a smart payment plan on large retail buys.

If saving on interest and getting rewards sounds appealing, reading further could bring fresh ideas—plus a few important cautions.

What Is a Store Credit Card With 0% Interest?

At its core, a store credit card is issued by a retailer, usually offering perks for purchases at their stores.

The “ 0% interest” part often applies as an introductory offer, covering a few months—or in some cases, over a year—where no interest is charged on purchases.

Many people use this period for big-ticket buys, like electronics or seasonal home makeovers, hoping to avoid extra costs. Of course, that sounds simple enough, but the reality can sometimes be more nuanced.

Why Consider Store Credit Cards With 0% Interest?

The appeal is obvious: Pay overtime, yet avoid interest (if you pay everything off before the period ends).

That said, it’s not just about deferring payments. Some folks see these cards as stepping stones to improved credit, or as a way to access member-only promos.

Potential Perks for Savvy Shoppers

- Interest-free financing for major purchases

- Special discounts, coupons, and exclusive events

- Points or rewards on store spending

- Easier approval odds than traditional credit cards, sometimes

Yet there’s a catch. Once the promo ends, rates tend to jump—often sharply. Anyone thinking long-term would do well to factor in these shifts, perhaps even setting reminders about payoff timelines.

Who Should Look Into Store Credit Cards With 0% Interest?

Students, first-time credit users, and those rebuilding their credit profile might find store cards appealing. Shoppers with planned, larger purchases may also benefit, as long as spending stays under control and repayments are timely.

But for anyone with a tendency to carry balances, traditional zero-interest balance transfer cards or personal loans might create less risk.

How 0% Interest Store Credit Card Offers Work

Most retailers offer an introductory period—often ranging between 6 and 24 months—where no interest accrues on qualifying purchases. Sometimes, it’s tied to a minimum spending amount. Maybe it’s a deferred interest offer, or perhaps a true 0% APR.

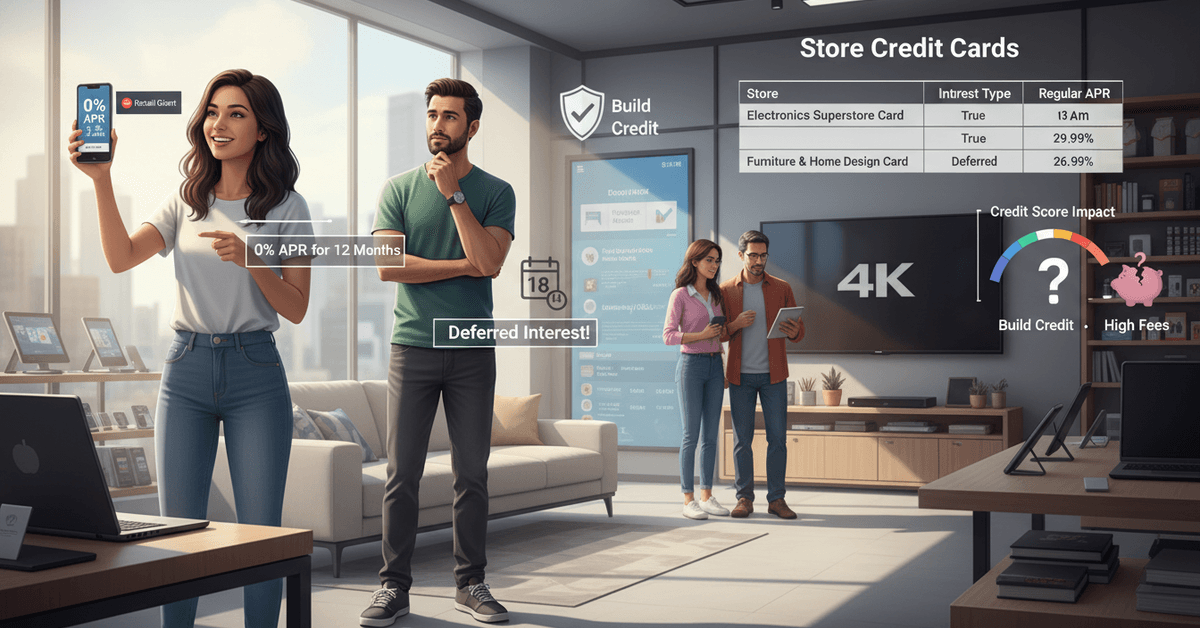

Deferred Interest vs. True 0% APR: The Difference

- True 0% APR: You won’t pay interest on purchases for the promo period, and only what remains after that gets new interest charges.

- Deferred interest: If the total isn’t paid off by the end, interest applies retroactively to the full purchase amount, from day one. This can be an expensive surprise.

Some stores are clear about which type they offer. Not all consumers catch the fine print, though. Perhaps that’s part of why complaints about retail credit card terms crop up now and again.

Top Store Credit Cards Offering 0% Interest in 2026

As with any financial product, the “best” choice truly depends on personal needs and shopping patterns.

A few major brands tend to lead the market, but regional stores sometimes roll out competitive offers, too. Here are some cards frequently mentioned for their 0% interest deals and generous terms:

Retail Giant Store Card

Available at one of the country’s most popular big-box chains. Many shoppers mention its occasional 12-month 0% APR financing on electronics and home goods.

Rewards include extra discounts and cash back events, but regular APR jumps significantly once the promo ends.

Department Store Preferred Card

Often found at major malls nationwide, this card is known for 6–18 month true 0% offers during seasonal sales. On top of the financing, members earn loyalty points usable on future purchases. Applicants sometimes report needing fair or better credit to qualify.

Furniture & Home Design Card

With a frequent 18-month deferred interest program (on qualifying purchases), this card is favored by folks planning big home updates.

The program has a strict on-time payment policy; missing even one payment could add hefty interest fees for the entire period.

Electronics Superstore Card

Well-suited for frequent tech shoppers, this card regularly features 0% intro offers on devices and accessories. Some buyers like the flexible repayment structure, and periodic access to “cardholder exclusive” sales events.

Online-Only Retailer Card

Perfect for those who mostly shop from home. Intro financing ranges up to 24 months on top-tier items. Approval is usually quick if you’re already a site member, but the regular APR can be high post-intro period.

Key Things to Consider Before Applying

The promotional headline can be tempting, but long-term costs should always be weighed. Some buyers realize, perhaps a little late, that fees and terms shift dramatically after the intro phase.

Application Impact

Applying for a new card generates a hard credit inquiry. For those seeking to improve their score, spacing out applications could help reduce the risk of denting credit reports.

Anecdotally, a bump or dip is common, but should even out after a few months if managed well.

Store Card Credit Limits

Store cards often come with lower starting limits when compared to general-purpose credit cards. This can be a mixed blessing: Yes, it encourages lower spending, but it might also impact credit utilization ratios—potentially affecting credit health.

Terms & Fine Print

This bears repeating: Always check if the 0% interest is deferred, or truly interest free. Consider autopay, or at least alerts, to avoid a missed payment. Those minor lapses can sometimes wipe out all the planned interest savings.

Alternatives to Store Credit Cards With 0% Interest

While 0% intro offers are tempting, they are not the only tool for financing big retail buys. For anyone looking to keep options open, there are a number of alternatives—each with their own set of trade-offs.

- Traditional 0% APR credit cards from banks and credit unions

- Buy Now, Pay Later services (like Afterpay or Klarna)

- Personal or installment loans with fixed monthly payments

Sometimes, the right strategy could be a mix—using a general 0% APR card for flexibility, while leveraging store cards for unique deals or points. Just watch for overlapping fees, of course.

Tips for Using Store Credit Cards Wisely

The riskiest outcomes often come from misunderstanding or forgetting the terms. A measured, attentive approach can help shoppers make the most of retail financing, while avoiding pitfalls that could add costs or harm credit in the long run.

Mark Promo End Dates

Set reminders for when the 0% offer expires. This prevents surprise interest charges—arguably one of the biggest draws for retail cards in the first place.

Pay On Time, Every Time

Missed or late payments may cancel out all the savings. Many shoppers rely on autopay to avoid these accidental slip-ups.

Know Your Spending Limits

Keeping balances comfortably below limits is generally good for credit health. Smaller purchases might build positive history without risking overspending.

Stay Aware of Changing Terms

Retailers can—and often do—change card terms or benefits. Reviewing updates, even occasionally, helps prevent surprises.

Conclusion

Store credit cards with 0% interest can help 2026 shoppers manage larger purchases, but only when the repayment plan is clear from the start.

The smartest strategy is to compare promo terms, avoid missed payments, and pay the balance before interest begins. Used carefully, retail financing can support planned spending without unnecessary debt.

Note: There are risks involved when applying for and using credit. Consult the bank’s terms and conditions page for more information.