The NatWest Nectar Credit Card has become a notable choice for many in the UK who are hoping to make everyday purchases a little more rewarding.

With rising living costs, any extra value—especially in the form of points that can be redeemed for shopping or travel—seems more appealing than ever.

This article unpacks how the NatWest Nectar Credit Card works, who might benefit, and how to get the most from its rewards in 2026.

If you’re thinking about credit card rewards, or just curious about how point-based systems work, this guide might offer some useful insights without the hard sell.

What Is the NatWest Nectar Credit Card?

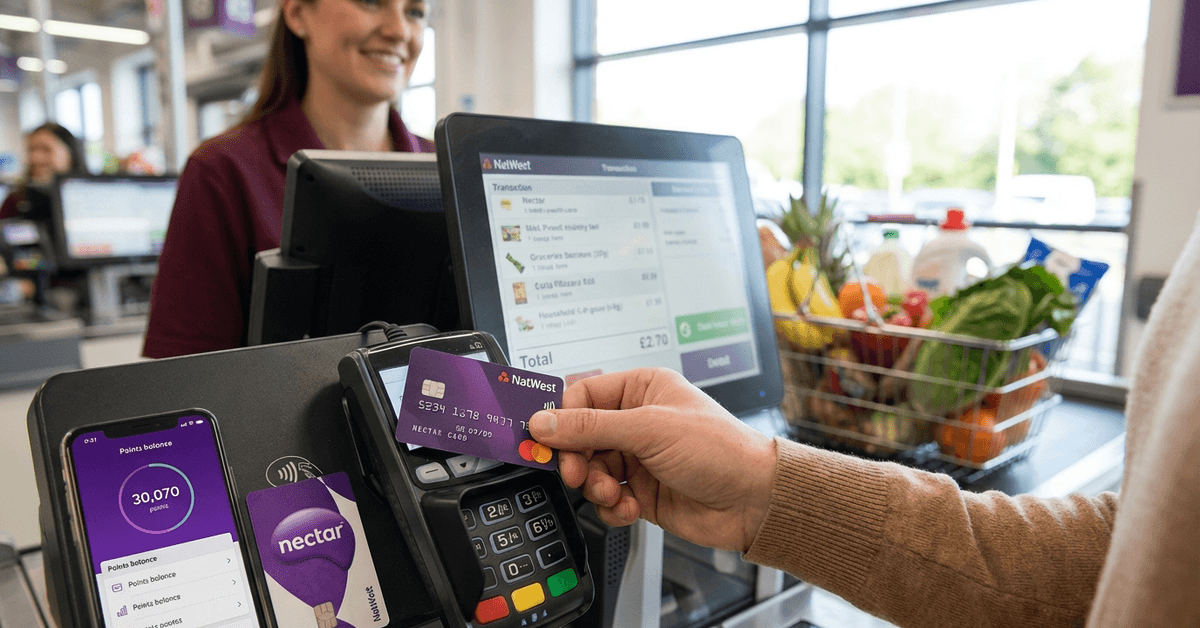

The NatWest Nectar Credit Card is a card that links your spending to the popular Nectar scheme, one of the UK’s largest loyalty programs.

Every eligible purchase you make, in theory, earns you Nectar points. These can later be converted into discounts or offers at certain retailers.

For people juggling everyday expenses—groceries, fuel, small treats—this approach to earning rewards could, perhaps, make a modest but noticeable impact over the course of a year. But is it always the right fit?

Core Features of the NatWest Nectar Credit Card

Earning Nectar Points on Purchases

One of the biggest features: every pound you spend on the card typically earns a set number of Nectar points.

Sometimes, special promotions might offer extra points for certain categories or partner retailers. However, the standard earn rate varies, and it's worth double-checking the current terms.

Annual Fee and Interest Rates

There’s sometimes an annual fee involved. Whether this fee is worth it largely depends on your spending patterns.

Interest rates apply to balances if not paid in full monthly, which could erode the benefit of any rewards if not managed carefully.

Nectar Partnership Benefits

The card is directly tied to the wider Nectar ecosystem. This means not just collecting points, but the potential to access bonus events, partner deals, or even unique experiences.

Still, these perks are subject to change, and some people might find they don’t use them as often as expected.

Who Might Benefit Most from the NatWest Nectar Credit Card?

Regular Nectar Users

If you already collect Nectar points—say, through Sainsbury’s, eBay, or other partners—you might find this card fits nicely into your shopping habits. The combination of supermarket points and card-based points can build up over time.

Loyalty-Driven Shoppers

There’s something satisfying about watching points accumulate and redeeming them for discounts. If you’re the type to organize your spending around loyalty schemes, this approach could be even more attractive.

Careful Budgeters

Since credit cards require disciplined repayment, those who pay their balance in full every month are likely to extract the most value.

Interest charges can erase rewards quickly if not managed, so regular budgeters might have an edge here.

Understanding the Nectar Reward System in 2026

Evolving Partner Network

Nectar’s list of partners has changed over the years. In 2026, frequent updates or changes might occur, with both classic brands and new digital platforms joining in.

Not every retailer on the high street—far from it—accepts Nectar, so occasional research helps.

Point Redemption

Nectar points can be used for things like groceries, fuel, or even experiences—though the real value depends on the redemption partner.

Sometimes, a special offer boosts point value. At other times, the return is more modest. Checking redemption options regularly can make a difference.

How to Apply for the NatWest Nectar Credit Card?

Eligibility Criteria

Applicants generally need to be UK residents over 18 with a reasonable credit history. Income requirements may vary.

The application will require personal details, financial information, and possibly existing Nectar account details for integration.

Digital Process

These days, most applications happen online. Decisions can be instant, though some cases take longer for assessment.

If you’re accepted, linking your card with your existing Nectar account streamlines the whole earning-and-redeeming process.

Comparing the NatWest Nectar Credit Card with Other Reward Cards

Nectar vs. Avios or Cashback

Choosing between different reward cards is rarely simple. Nectar points are flexible across several partners, but travel reward cards (like those offering Avios) might suit frequent flyers.

Meanwhile, cashback cards rebate a percentage of spending as cash instead of points. Which style appeals may come down to personal habits, or even just a gut feeling about value.

Annual Fee Comparison

Some reward cards are fee-free, while others (including the NatWest Nectar) may charge an annual fee.

The best value often comes when the total points or benefits clearly outweigh the fee over 12 months. This rarely happens automatically; tracking spending is surprisingly important.

Interest-Free Offers and Balance Transfer Options

Card providers sometimes introduce introductory offers, like interest-free purchases or balance transfers.

While tempting, these offers have limitations and sometimes strict criteria. It’s probably wise not to chase them unless genuinely beneficial—otherwise, the regular APR will eventually apply.

Tips for Maximizing Nectar Points and Card Value in 2026

Strategic Spending Habits

- Using the card for all everyday, budgeted expenses could boost point totals without extra effort.

- Avoid impulse purchases just for points—it’s not usually worth it.

- Combine Nectar collection through the card and partner retailers for the best results.

Clearing Balances Monthly

- Interest charges often cancel out rewards. Paying your balance in full every month is one of the simplest ways to extract real benefit from any reward credit card.

Track Promotional Offers

- Nectar and NatWest frequently introduce double-points events or partner bonuses. While it could seem like minor gains, over the course of a year, these little boosts may add up.

- Sign up for notifications or check the app regularly.

Security and Responsible Use

Safe Online Purchases

Credit cards, including this one, offer certain online shopping protections, like Section 75 cover for larger purchases.

Still, while the additional layer of security is reassuring, a cautious approach to new or unfamiliar retailers could avoid headaches.

Managing Credit Limits

The limit you’re offered depends on financial history and income. Staying within the assigned threshold safeguards both your credit score and any eligibility for future offers—or even for a credit limit increase. Overspending leads to fees, so keeping an eye on balances feels essential.

Legal and Tax Considerations for Nectar Credit Cards

Personal vs. Business Spending

For most people, points earned are a personal benefit and don’t have tax implications. However, if the card is used for business expenses, sometimes there are reporting requirements or employer guidelines. Professional advice might be needed if business use is frequent.

Consumer Rights

UK credit agreements include mandatory protections, but terms can change with new regulations. Reading updated small print—especially regarding fees or reward changes—can help sidestep surprises. It's not fun reading, but sometimes it’s necessary.

Frequently Asked Questions about NatWest Nectar Credit Card

Where can Nectar points be spent?

Points can typically be redeemed with Sainsbury’s, Argos, eBay, and other Nectar partners. The full partner list is available on the Nectar website. Redemption value might vary based on the retailer or current offers.

Is there a minimum spend for earning Nectar points?

Every eligible pound spent usually earns points, but some merchants or transaction types may be excluded. Checking the card’s latest reward guide clarifies which transactions qualify.

What if the annual fee goes up?

Credit card issuers notify cardholders before making changes to annual fees or terms. Reviewing communication from NatWest helps keep track of any adjustments that could affect the card’s value proposition.

Final Thoughts

The NatWest Nectar Credit Card can offer useful value for people who already collect Nectar points regularly.

Its real benefit depends on disciplined spending, full monthly repayment, and smart use of partner offers.

Annual fees and interest can quickly reduce the rewards if the card is not managed carefully. For the right user, though, it can make everyday spending feel a little more rewarding over time.